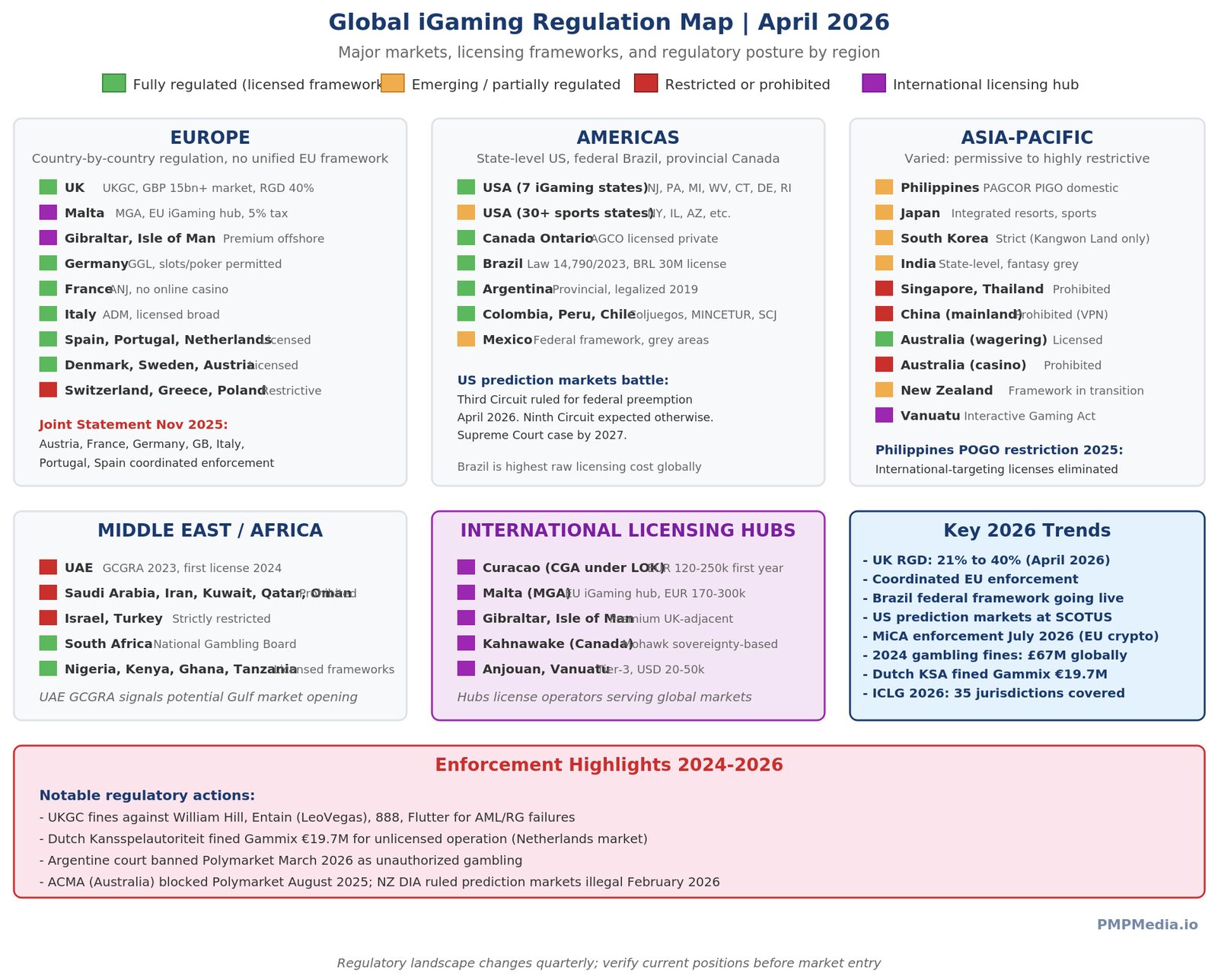

Global iGaming regulation in 2026 is more fragmented, more active, and more consequential for operators than ever before. The coordinated enforcement push by major European regulators in late 2025, the US Supreme Court situation around prediction markets, Brazil’s federal licensing framework going into full effect, and continued tightening across most mature markets make this a genuinely transitional period in how online gambling is governed worldwide.

This guide provides a comprehensive country-by-country analysis of iGaming regulation in 2026. It covers the major regulated markets, emerging frameworks, restricted jurisdictions, and the regulatory trends shaping operator decisions globally. Written for legal counsel, compliance professionals, investors, and operators evaluating international market strategy. For foundational concepts, see our what is a gambling license guide. For practical licensing process, see our iGaming licensing guide. For license category classification, see types of gambling licenses.

The Global Regulatory Picture in 2026

Four broad regulatory categories exist globally in 2026:

Fully regulated markets: National or state frameworks with licensed operators, active supervision, and enforcement. Most of Europe, major US states, UK, Canada Ontario. Operators need local licensing to serve these markets.

International licensing hubs: Jurisdictions that license operators serving global markets but where local populations may or may not participate. Curacao, Malta, Gibraltar, Isle of Man, Anjouan, Kahnawake.

Partially regulated or developing markets: Countries with emerging frameworks where licensing exists but is still establishing. Brazil, Argentina, Philippines, emerging LATAM, UAE.

Restricted or prohibited markets: Countries where online gambling is either explicitly banned (Saudi Arabia, Iran, China) or tightly restricted (Singapore, Thailand, Taiwan).

The regulatory picture has been consolidating around stricter enforcement in fully regulated markets while emerging markets develop their own frameworks. Unlicensed operation increasingly faces enforcement pressure. The November 25, 2025 joint enforcement statement by Austria, France, Germany, Great Britain, Italy, Portugal, and Spain explicitly committed these jurisdictions to coordinated action against unlicensed operators targeting their consumers.

Europe: Fragmented but Tightening

Europe has no unified iGaming regulation. Each EU member state regulates gambling at the national level, producing a patchwork of frameworks that operators must navigate country-by-country. The EU provides horizontal frameworks (GDPR, AML Directives, MiCA for crypto) but individual gambling regulation is national.

United Kingdom

The world’s largest single regulated online gambling market, with GGY exceeding GBP 15 billion annually. Regulated under the Gambling Act 2005 by the UK Gambling Commission. Point-of-consumption taxation means any operator serving UK customers needs a UKGC license.

Major 2026 changes: Remote Gaming Duty raised from 21% to 40% effective April 1, 2026. General Betting Duty new 25% rate for remote bets. Proposed 30% increase in UKGC operating license fees from October 2026. Continued implementation of 2023 White Paper reforms including financial vulnerability checks, online slot stake limits, and statutory levy.

The UK remains mandatory for UK customers with no practical alternative. See our detailed UK Gambling License guide.

Malta

EU iGaming hub. Malta Gaming Authority (MGA) regulates online gambling with the most established EU-wide recognized license. Malta licenses are respected globally and often required for serving multiple EU markets indirectly.

Framework: 5% gaming tax on online gaming revenue. Multi-tier license types (Type 1-4). Application fee EUR 5,000, annual fee EUR 25,000-35,000. Strong AML requirements, responsible gambling obligations, and ongoing compliance supervision.

Malta continues to position as the EU premium jurisdiction with strong banking relationships and institutional credibility. See our Malta Gaming License guide.

Germany

The largest EU economy with one of the most complex gambling frameworks. The Interstate Treaty on Gambling (Glücksspielstaatsvertrag, GlüStV 2021) establishes unified framework across all 16 federal states.

Regulator: Gemeinsame Glücksspielbehörde der Länder (GGL), the Joint Gambling Authority of the German Federal States. Online slot machines and online poker are permitted under strict monthly deposit limits and stake caps. Online casino table games (blackjack, roulette) remain restricted. Sports betting permitted with licensing.

2026 enforcement focus: The GGL and German federal states are tightening enforcement against unlicensed operators. Amendments to GlüStV 2021 in progress to enable ISP-level blocking of illegal sites. Joint enforcement statement signatory.

France

Autorité Nationale des Jeux (ANJ) regulates online gambling. Sports betting, horse racing, and poker are permitted; casino games remain prohibited for online operators. ANJ has been aggressive in enforcement against unlicensed prediction markets and offshore operators serving French consumers.

Joint enforcement statement signatory. Prohibitive posture toward unlicensed operations.

Italy

Agenzia delle Dogane e dei Monopoli (ADM), part of the Ministry of Finance, oversees Italian gambling. Regulates online casino, poker, sports betting, and lotteries. License system well-established, with 800+ licensed operators in the regulated market.

Joint enforcement statement signatory. Italian tax rates for online gambling are among the highest in Europe (25% on casino GGR, various rates on sports betting).

Spain

Dirección General de Ordenación del Juego (DGOJ) regulates online gambling. Licensed casino, poker, sports betting, and bingo. Strong marketing restrictions (limits on advertising, promotional activities).

Joint enforcement statement signatory. Some operators explicitly choose Spain for regulatory clarity, others find compliance costs challenging.

Netherlands

Kansspelautoriteit (KSA) regulates Dutch online gambling. Framework went into effect in 2021 with online casino and sports betting licensing. Known for aggressive enforcement action — the Dutch regulator has fined numerous operators for serving Dutch consumers without Dutch license, including record EUR 19.7 million fine against Gammix.

Remote gambling operators need local Dutch license; international licenses do not suffice. Strict advertising restrictions.

Denmark

Spillemyndigheden (Danish Gambling Authority) regulates online gambling. Framework established in 2012 with licensed operators serving Danish customers. Typical costs: DKK 257,000 application fee (approximately EUR 34,400), DKK 50,000 annual fee. Strong reputation for player protection and responsible gambling.

Sweden

Spelinspektionen regulates Swedish gambling under Gambling Act 2018. Licensed framework including casino, sports betting, and lotteries. SEK 700,000-800,000 application fees depending on license type. 18% gambling tax.

Sweden has seen operator exits and re-entries as regulatory costs and commercial reality aligned. Current framework stable.

Austria

Gambling regulation under Glücksspielgesetz (GSpG). Lotteries and casino under federal framework; sports betting regulated by the nine Federal Provinces (Bundesländer) because Austria classifies it as skill-based, not chance. Federal Ministry of Finance (BMF) oversees federal licensing.

Joint enforcement statement signatory. Notable for distinctive treatment of sports betting separate from gambling law.

Portugal

Serviço de Regulação e Inspeção de Jogos (SRIJ) of Turismo de Portugal regulates online gambling. Casino, sports betting, and poker permitted with licensing. Marketing restrictions apply.

Joint enforcement statement signatory. 2026 investigation of prediction market operations (Polymarket) during Portuguese presidential election raised insider trading concerns.

Belgium

Gaming Commission regulates Belgian gambling. Framework requires operators to have Belgian physical establishment to offer certain products (restrictive for international operators). Strict regulation with lower tolerance for offshore operators.

Ireland

Gambling Regulation Act 2024 established new regulatory framework, with Gambling Regulatory Authority of Ireland (GRAI) now regulating. Transition to new framework ongoing through 2026. Previously operators served Irish market under UK licensing or Malta licensing.

Gibraltar

Gibraltar Gambling Commission operates under Gambling Act 2005. Long-established jurisdiction serving UK market historically. Strong banking and payment infrastructure. EUR 25,000 one-time license fee, moderate annual fees.

March 2026: Gibraltar became first European jurisdiction to license a prediction market operator (PredictStreet), demonstrating willingness to develop innovative licensing frameworks.

Smaller and emerging EU markets

- Poland: Totalizator Sportowy and Ministry of Finance regulate. Strict restrictions; most foreign operators blocked

- Romania: ONJN (National Gambling Office) regulates. Moderately open licensing framework

- Czech Republic: Ministry of Finance regulates. Established framework with moderate licensing costs

- Bulgaria: National Revenue Agency regulates. Framework tightening since 2020

- Greece: Hellenic Gaming Commission. Restrictive framework; most offshore operators blocked

- Finland: Veikkaus has historical monopoly but reform planned for 2026-2027

- Norway: Norsk Tipping monopoly; EU-adjacent but not EU member

- Switzerland: Swiss Federal Gaming Board regulates. Restrictive; online casinos must be land-based casino operators

- Estonia, Latvia, Lithuania: Licensed frameworks with varied levels of strictness

North America

United States (federal framework)

US federal gambling law is fragmented. Three main federal statutes:

- Wire Act (1961): DOJ interpretation has shifted; 2019 reinterpretation applies only to sports betting; earlier interpretations applied to all gambling

- Unlawful Internet Gambling Enforcement Act (UIGEA, 2006): Prohibits processing payments for unlawful internet gambling

- Professional and Amateur Sports Protection Act (PASPA, 1992): Struck down by Supreme Court Murphy v. NCAA 2018, giving states authority over sports betting

State-by-state licensing dominates. Tribal gaming operates under Indian Gaming Regulatory Act (IGRA) framework with state-tribal compacts.

US iGaming states (as of April 2026)

Seven states have legalized online casino (iGaming): New Jersey, Pennsylvania, Michigan, West Virginia, Connecticut, Delaware, and Rhode Island. These markets generated approximately USD 8.4 billion in gross gaming revenue collectively in recent year.

New Jersey is the largest and most established iGaming market, with Division of Gaming Enforcement (DGE) as regulator. USD 400,000 casino license fee. Pennsylvania Gaming Control Board (PGCB) has higher fees (up to USD 10 million for casino operators). Michigan Gaming Control Board (MGCB) fast-growing.

US sports betting states

30+ states have legalized sports betting since PASPA repeal in 2018. Largest by revenue: New York, New Jersey, Pennsylvania, Illinois, Arizona. Some states offer full online operation; others restrict to in-person registration or retail-only.

US prediction markets regulatory battle

CFTC-registered prediction markets (Kalshi, Polymarket US via QCX) claim federal exclusive jurisdiction over event contracts. State gambling commissions (Massachusetts, Nevada, Arizona, Connecticut, Illinois, Maryland, New Jersey, Washington State) argue sports contracts are gambling regardless of CFTC status. Third Circuit ruled for federal preemption in April 2026 KalshiEX v. Flaherty; Ninth Circuit expected to rule differently. Supreme Court case likely by 2027.

Canada

Federal Criminal Code prohibits gambling unless authorized by provincial law. Provincial-level regulation:

- Ontario: AGCO (Alcohol and Gaming Commission of Ontario) regulates private online gambling. Model for other Canadian provinces. Over 70 licensed operators

- British Columbia, Quebec, Alberta: Crown-corporation models (BCLC, Loto-Quebec, AGLC) with monopoly status

- Other provinces: Mixed approaches, Atlantic Lottery Corporation serves several eastern provinces

Ontario’s private operator model is the most open. Other provinces maintain monopoly structures.

Mexico

Ministry of Interior regulates gambling under Federal Gaming and Raffles Law (1947). Regulatory framework creating uncertainty. Operators typically structure through Mexican-licensed casinos or operate in regulatory grey area.

Latin America

Brazil

Most important new regulated market in global iGaming. Federal Law 14,790/2023 established modern licensing framework that went into effect 2024-2025. Federal regulator SPA (Secretaria de Prêmios e Apostas) under Ministry of Finance.

Key framework elements:

- License fee: BRL 30 million (approximately USD 5.5-6.1 million) for 5-year federal authorization

- Monthly supervisory fee based on GGR, up to BRL 1.9 million per month for largest operators

- .bet.br domain mandatory for Brazilian-licensed operators

- 18% gambling tax on operator revenue

- Integration with official government monitoring system required

- Responsible gambling obligations including AML and KYC aligned with FATF

- Corporate presence in Brazil required

Brazil is the highest raw licensing cost in global iGaming but offers access to Latin America’s largest economy with tens of millions of potential customers. Over 100 operators have obtained licenses or provisional authorizations.

Argentina

Legalized online gambling in 2019; licenses issued from 2021. Regulated at provincial level with most activity in Buenos Aires, Mendoza, Santa Fe. Argentine Lottery (Lotería de la Ciudad) and provincial lottery agencies regulate.

Significant 2026 development: Argentine court banned Polymarket as unauthorized gambling operation in March 2026, signaling regulatory tightening against unlicensed operators.

Colombia

Coljuegos (National Gambling Regulator) regulates. Licensed online gambling including casino, poker, and sports betting. First Latin American country with federal iGaming regulation. Known for relatively stable regulatory environment.

Peru

Ministry of Foreign Trade and Tourism (MINCETUR) through DGJCMT (General Directorate of Games of Chance) regulates. New Law 31557 (2022) established licensing framework for online gambling. Transition ongoing through 2026.

Chile

Superintendence of Casinos of Games (SCJ) regulates land-based casinos. Online gambling operates in regulatory grey area pending specific framework. Framework development expected through 2026-2027.

Other LATAM markets

- Mexico, Panama, Costa Rica: Mixed frameworks, often lighter regulatory touch

- Ecuador, Bolivia: Largely restrictive

- Uruguay: State-run monopoly

- Venezuela: Significant operational challenges despite legal framework

Asia

Asia has the most varied regulatory landscape globally, with strict prohibition in some markets and open commercial markets in others.

Philippines

Philippine Amusement and Gaming Corporation (PAGCOR) is the regulatory and licensing authority. Significant 2025 changes: Offshore Gaming Operations (POGO/OGI) targeting international players were substantially restricted or effectively eliminated by 2025. Philippine Inland Gaming Operators (PIGO) license now focuses on domestic market.

Minimum paid-up capital around PHP 25 million (approximately USD 429,000+) depending on license type. PIGO licensing is the primary framework for domestic-focused operations.

Japan

Integrated Resort Implementation Act (2018) authorizes three integrated resorts with casino gaming. Horse racing, boat racing, motorcycle racing, bicycle racing, and sports lottery are permitted. Other gambling is generally restricted. Online casino remains prohibited for domestic operators but access by consumers to offshore operators exists.

South Korea

Strict prohibition on gambling for Korean citizens. Only Kangwon Land casino permits Korean nationals. Foreign-targeted casinos operate (Paradise, Grand Korea Leisure). Online gambling is prohibited but enforcement varies.

India

State-by-state regulation. Some states (Goa, Sikkim) permit certain forms of gambling; others prohibit entirely. Online fantasy sports operates in grey area with ongoing court challenges. National-level framework lacking. Large market potential unlocked with clearer regulation.

Singapore

Strict Remote Gambling Act. Prohibited except for exempt operators (Singapore Pools for lottery and sports betting). Aggressive enforcement including geoblocking of unlicensed operators. Not a market for offshore operators.

Thailand

Prohibition on all forms of gambling except state lottery and horse racing at specific venues. Legislation development underway for potential casino legalization, but online gambling remains restricted.

Taiwan

Gambling generally prohibited under Criminal Code. Offshore operators geoblocked. Not a licensed market for commercial iGaming.

China

Mainland China prohibits all gambling except state lotteries and sports lottery. Macau and Hong Kong have separate regulatory regimes (Macau has world’s largest gaming revenue through land-based casinos). Online gambling geoblocked across mainland.

Other Asia

- Vietnam: Limited legal gambling; foreigners-only policy for most venues

- Cambodia, Laos: Casino-friendly for tourism; online gambling ambiguous

- Malaysia: Strictly prohibited except at Genting Highlands

- Indonesia: Prohibited

Oceania

Australia

Interactive Gambling Act 2001 prohibits most online gambling by Australians. Licensed online wagering (sports betting, lotteries) permitted. Online casino games are illegal for Australian customers. Strict advertising restrictions.

ACMA (Australian Communications and Media Authority) enforces illegal online gambling provisions including ISP-level blocking. In August 2025, ACMA specifically blocked Polymarket for serving Australian customers. Enforcement continues to tighten.

New Zealand

Department of Internal Affairs (DIA) regulates under Gambling Act 2003. TAB holds monopoly over online sports betting. February 2026 ruling: DIA formally prohibited prediction markets like Polymarket and Kalshi under Gambling Act 2003 and Racing Industry Act 2020.

Online Casino Gambling Bill is progressing, auctioning 15 online casino licenses — creating limited framework for regulated online casino operation.

Pacific Islands

- Fiji: Local licensing for online gambling operators serving Fiji market

- Vanuatu: Interactive Gaming Act 2000 provides permissive regulatory framework; used as licensing jurisdiction for international operators

- Cook Islands, Samoa: Small licensing roles

Middle East and Africa

United Arab Emirates

Historically prohibited gambling under Islamic law. Significant 2023 development: General Commercial Gaming Regulatory Authority (GCGRA) established. First lottery license awarded in July 2024. Signals potential opening of limited gaming in UAE, though mass-market online gambling remains restricted.

Saudi Arabia, Iran, Kuwait, Bahrain, Qatar, Oman

Gambling prohibited under Islamic law. Strict enforcement. Not markets for commercial iGaming operations.

Israel

Monopoly through state lotteries. Private commercial gambling prohibited. Online gambling not legally available for Israeli citizens.

Turkey

Gambling generally prohibited outside state lotteries. Enforcement includes ISP blocking of offshore gambling sites.

Africa

- South Africa: Regulated framework through National Gambling Board. Licensed operators for domestic market

- Nigeria: Lagos State Lotteries and Gaming Authority provides framework for sports betting. Regulated market

- Kenya: Betting Control and Licensing Board regulates. Liberalized market with licensed operators

- Ghana: Gaming Commission regulates. Moderate framework

- Tanzania: Gaming Board of Tanzania regulates sports betting and lottery

- Egypt, Tunisia, Morocco: Limited gambling legality; mostly tourism-oriented land-based

Major Regulatory Themes in 2026

Coordinated enforcement against unlicensed operators

The November 25, 2025 Joint Statement by Austria, France, Germany, Great Britain, Italy, Portugal, and Spain committed these jurisdictions to coordinated action against unlicensed operators. Key elements include information sharing, calls on digital platforms to limit advertising of unauthorized operators, and commitment to strengthen ISP and payment blocking. Individual regulators continue to issue substantial fines.

Rising compliance expectations

Regulators increasingly expect substantial compliance infrastructure: robust AML, KYC, transaction monitoring, responsible gambling tools, affordability checks, and detailed reporting. Template policies that satisfied earlier regulators no longer suffice.

Advertising restrictions intensifying

Most mature markets have been tightening advertising rules. UK requires opt-in consent for direct marketing. Spain, Italy, and Germany have increasingly restrictive advertising frameworks. Belgium introduced near-total advertising ban. Netherlands restricts times when gambling ads can air. Affiliate marketing regulation is also tightening.

Tax rate increases

Multiple mature markets have raised gambling tax rates. UK Remote Gaming Duty increased from 21% to 40% in April 2026. Italy maintains 25% on casino GGR. Nordic markets generally 18-20%. This trend of raising tax rates while tightening compliance is making some markets less attractive for operators while benefiting larger established players who can absorb the cost.

Financial crime focus

AML enforcement has been aggressive. 2024 gambling industry faced approximately £67 million in global regulatory penalties, with significant cases including Entain, William Hill, 888, and others. Dutch Gaming Authority fined Gammix €19.7 million for unlicensed operation. UK, Dutch, and German regulators have been particularly active.

Crypto gambling regulatory tightening

Crypto-accepting gambling operators face increasing AML scrutiny. Curacao under LOK requires chain analysis tools and FATF-aligned compliance. MiCA in EU adds crypto-specific requirements for gambling operators using cryptocurrency. Anonymous crypto casino operations increasingly restricted.

Prediction markets emergence

US CFTC-regulated prediction markets (Kalshi, Polymarket US) have created new category bridging gambling and financial markets. UK treats these as betting under UKGC (Matchbook Predictions, Betfair Predicts in 2026). EU member states mostly classify as gambling and require local licensing. Supreme Court case expected by 2027 may reshape US framework. For the complete analysis of this emerging category, see our dedicated prediction markets regulation guide.

US CFTC-regulated prediction markets (Kalshi, Polymarket US) have created new category bridging gambling and financial markets. UK treats these as betting under UKGC (Matchbook Predictions, Betfair Predicts in 2026). EU member states mostly classify as gambling and require local licensing. Supreme Court case expected by 2027 may reshape US framework.

State-level US regulatory complexity

US operations face 50+ separate state regulatory ecosystems. Multi-state operators manage substantially different requirements in each state. Geolocation compliance, KYC thresholds, responsible gambling rules, and reporting cadence vary by state. Operational complexity is high and compliance costs scale with state count.

Brazilian market maturation

Brazil’s framework rollout has been the most significant new regulatory development in Latin America. BRL 30 million license fees plus monthly supervisory fees create high barriers to entry but the market size (tens of millions of potential customers) justifies investment for well-capitalized operators.

ICLG 2026 coverage

The International Comparative Legal Guide to Gambling Laws and Regulations 2026 (ICLG) covers 35 jurisdictions with detailed analysis of each regulatory framework. This reference provides the most comprehensive jurisdiction-by-jurisdiction comparative analysis and is updated annually with current regulatory positions.

Strategic Implications for Operators

For new market entrants

Target market selection drives everything else. Match license strategy to target customer geography. Budget for local licensing in each target market; do not assume international licenses will work. Compliance costs are rising faster than revenue in many markets.

For established operators

Portfolio review is increasingly important. Some jurisdictions that made sense 3 years ago have become less attractive due to tax increases or tightening compliance. Others (Brazil, specific US states) offer new opportunities with high barriers to entry.

For investors and acquirers

Regulatory posture materially affects valuation. Operators with clean multi-jurisdiction licensing trade at premiums to offshore-only operators. Regulatory issues in one market can affect access to others. Due diligence must include detailed regulatory review.

For service providers and B2B

Compliance partner opportunities continue to expand as operators need help meeting rising standards. Technical certification labs, compliance consultancies, legal advisors, and technology providers serve the entire ecosystem.

The 2026-2027 Outlook

Several developments will shape global iGaming regulation over the next 12-24 months.

US prediction markets Supreme Court ruling

Expected 2027 Supreme Court resolution on federal preemption for CFTC-registered event contracts. Either outcome is consequential. Pro-federal ruling unlocks nationwide expansion. Pro-state ruling forces compliance with state gambling frameworks.

UK tax impact

Full year impact of 40% Remote Gaming Duty and proposed October 2026 fee increases will reshape UK iGaming profitability. Some consolidation expected as smaller operators struggle with the cost structure.

Brazil market establishment

Brazilian regulated market maturation through 2026-2027 as operators launch under Law 14,790/2023. Initial winners likely to be well-capitalized operators who can bear high licensing costs.

EU MiCA impact

Full MiCA enforcement from July 2026 affects crypto-using gambling operators across EU member states. Added compliance layer on existing gambling regulations.

Joint enforcement action escalation

The November 2025 joint statement signatories likely to escalate coordinated enforcement against unlicensed operators through 2026-2027. Payment blocking, ISP blocking, and advertising restrictions expected to tighten.

Additional US state markets

New York iGaming legislation, California and Texas sports betting expansion all possible through 2026-2027. Each unlocks substantial market opportunity with state-specific licensing.

Philippines domestic market consolidation

Post-POGO restriction environment solidifying. PIGO licensees competing for domestic Philippine market with restrictions on international targeting.

UAE market development

GCGRA framework continues development. Additional license types may emerge through 2026-2027 representing significant regulatory change in the Gulf region.

Related Guides

- What Is a Gambling License

- Types of Gambling Licenses

- iGaming Licensing Guide

- Malta Gaming License

- Curacao iGaming License

- UK Gambling License

- Curacao License Requirements

- Curacao License Cost

- Curacao vs Malta License

Bottom Line

Global iGaming regulation in 2026 is characterized by fragmentation, active enforcement, and rising compliance expectations. No single framework applies globally. Operators serving international markets need jurisdiction-specific strategies, multiple licenses, and substantial compliance infrastructure.

The regulatory direction of travel is clearly toward stricter enforcement, higher taxes in mature markets, and reduced tolerance for unlicensed operation. Markets that historically operated in regulatory grey areas are either moving toward formal regulation (Brazil, UAE, various emerging markets) or tightening enforcement against offshore operators (EU coordinated action, UK, Netherlands).

The winners in this environment are operators who treat regulation as core strategic infrastructure rather than as a cost center. Sustained investment in compliance, legal advisors, and multi-jurisdiction licensing supports long-term business value. Operators trying to arbitrage regulatory weaknesses face increasing enforcement pressure and commercial limitations from banking and payment partners.

FAQ

Which countries allow online gambling in 2026?

Major regulated markets in 2026 include: United Kingdom, Malta, Germany, France, Italy, Spain, Netherlands, Denmark, Sweden, Portugal, Austria, Gibraltar, Isle of Man, Brazil, Argentina, Colombia, Peru, Mexico, Philippines, South Africa, Kenya, Ontario Canada, and seven US states (NJ, PA, MI, WV, CT, DE, RI) with more states for sports betting only. Each has its own licensing framework.

Which countries prohibit online gambling?

Major prohibition jurisdictions include Saudi Arabia, Iran, Kuwait, Bahrain, Qatar, Oman (Islamic law), Thailand, China mainland, Indonesia, Singapore, Taiwan, and most Gulf states. Some allow limited state-operated gambling (lotteries) but prohibit commercial operators. Enforcement varies but is generally strict.

Do I need separate licenses for each country?

In most cases yes. Most countries operate point-of-consumption regulation, requiring local licensing for any operator serving local consumers. International licenses (Malta, Curacao) provide access to some markets but cannot replace national licensing in most regulated jurisdictions. Operators serving multiple markets typically hold multiple licenses.

Which is the most respected gambling license in the world?

UK Gambling Commission (UKGC) is generally considered the most rigorous and respected globally, due to strict enforcement, detailed regulatory framework, and mature market. Malta Gaming Authority (MGA) is considered the leading EU-wide recognized license. Gibraltar, Isle of Man, and Alderney are also highly regarded. These Tier-1 licenses carry strongest banking credibility and institutional recognition.

What is the Joint Statement on illegal gambling?

On November 25, 2025, gambling regulators for Austria, France, Germany, Great Britain, Italy, Portugal, and Spain issued a joint statement committing to coordinated action against illegal online gambling. The statement calls for information sharing on illegal operators, pressure on digital platforms to restrict advertising of unauthorized operators, and strengthened enforcement mechanisms. Signals increasing coordination among European regulators.

How is Brazil regulating iGaming?

Brazil established modern federal licensing framework under Law 14,790/2023. License fee: BRL 30 million (approximately USD 5.5-6.1 million) for 5-year authorization. Monthly supervisory fee based on GGR, up to BRL 1.9 million per month. Mandatory .bet.br domain. 18% gambling tax. Full operational presence required. Highest raw licensing cost globally but access to Latin America’s largest market.

What is happening with prediction markets regulation globally?

US: CFTC-regulated prediction markets (Kalshi, Polymarket) claim federal jurisdiction; multiple states argue sports contracts constitute gambling. Third Circuit ruled for federal preemption April 2026. Supreme Court case expected by 2027. UK: treated as betting under UKGC (Matchbook Predictions launched January 2026, Betfair Predicts April 2026). EU: mostly classified as gambling requiring national licensing. Gibraltar licensed PredictStreet as first European prediction market operator in March 2026.

What countries have the highest gambling taxes?

UK has the highest remote gambling tax: Remote Gaming Duty increased from 21% to 40% in April 2026. Italy has 25% on casino GGR. Nordic countries (Denmark, Sweden) at 18-20%. Germany varies by product. France, Netherlands have high effective rates. Curacao remains at 2% on GGR. Brazil at 18%. US state taxes vary widely (15-35%+ depending on state and product).

Is China planning to legalize online gambling?

No indications of changes to current prohibition. Mainland China prohibits all gambling except state lotteries. Hong Kong and Macau have separate regimes (Macau has the world’s largest gaming revenue market through land-based casinos). No federal-level movement toward online gambling legalization in 2026.

What is the status of iGaming in the United Arab Emirates?

Significant 2023 development: UAE established General Commercial Gaming Regulatory Authority (GCGRA) to oversee commercial gaming. First lottery license awarded in July 2024. Framework continues to develop through 2026. Full online casino gambling for mass market not yet available, but the regulatory infrastructure is being built. Commercial gaming is developing in a region previously defined by strict prohibition.

How does EU MiCA affect iGaming operators?

MiCA (Markets in Crypto-Assets) regulation reaches full enforcement from July 2026 in EU member states. Gambling operators using cryptocurrency (Bitcoin, Ethereum, stablecoins) are subject to MiCA requirements including Crypto-Asset Service Provider licensing, market abuse rules, and transaction monitoring. Adds compliance layer on top of existing gambling regulations in member states. Mandatory for any crypto-accepting operator serving EU customers.

What is happening in the Philippines iGaming market?

Significant 2025 changes. POGO/OGI licenses targeting international players were substantially restricted or effectively eliminated. PAGCOR licensing now focuses on PIGO (Philippine Inland Gaming Operators) for domestic market. Minimum paid-up capital approximately PHP 25 million (USD 429,000+) depending on license type. Domestic Philippine market continues but international-focused operators must look elsewhere.

Share

Share

0 views

0 views

Analysis

Analysis  Business

Business  Companies

Companies  Crime

Crime  Finance

Finance  M&A

M&A  Prediction Markets

Prediction Markets  Regulation

Regulation  Reports

Reports