Prediction markets regulation is the most unsettled topic in financial services right now. The US has federal clarity under the CFTC, but multiple states are suing prediction market operators anyway. The UK treats them as gambling under the Gambling Commission. France, Germany, the Netherlands, Belgium, Portugal, Italy, Poland, and several others have explicitly banned the major platforms. Australia has blocked access through ISPs. New Zealand ruled them illegal in February 2026. Brazil has not decided yet. A US Supreme Court case is increasingly likely by 2027.

This guide explains how prediction markets are currently regulated across major jurisdictions, why the legal classification is genuinely contested, what the ongoing court battles mean for the industry, and where regulation is likely to go over the next 18 months. Written for operators, investors, and industry professionals who need to understand the landscape rather than a consumer-style legal Q&A. For a broader industry overview, see our prediction markets guide. For the foundational basics of how these platforms work, start with what are prediction markets.

The Core Regulatory Question

The fundamental debate in prediction markets regulation comes down to a single question: are these financial instruments or gambling products?

The answer has enormous consequences. Financial instruments get regulated by securities and commodities authorities, usually at the federal or supranational level, with frameworks built around market integrity, disclosure, and investor protection. Gambling products get regulated by gaming commissions at the state or national level, with frameworks built around consumer protection, problem gambling, and integrity monitoring.

Prediction markets have structural features of both. They use exchange-based order books like financial markets. They let participants speculate on event outcomes like sportsbooks. The prices reflect probability like derivatives. The contracts resolve to a fixed payout like fixed-odds bets. Reasonable regulators looking at the same product can reach opposite conclusions, and in 2026 they consistently do.

The US has chosen the financial instrument path at the federal level, with the CFTC claiming exclusive jurisdiction. Most of Europe, Australia, and New Zealand have chosen the gambling path. That divergence is not temporary. It reflects genuine disagreement about how to classify a product that was not contemplated when the relevant legal frameworks were written.

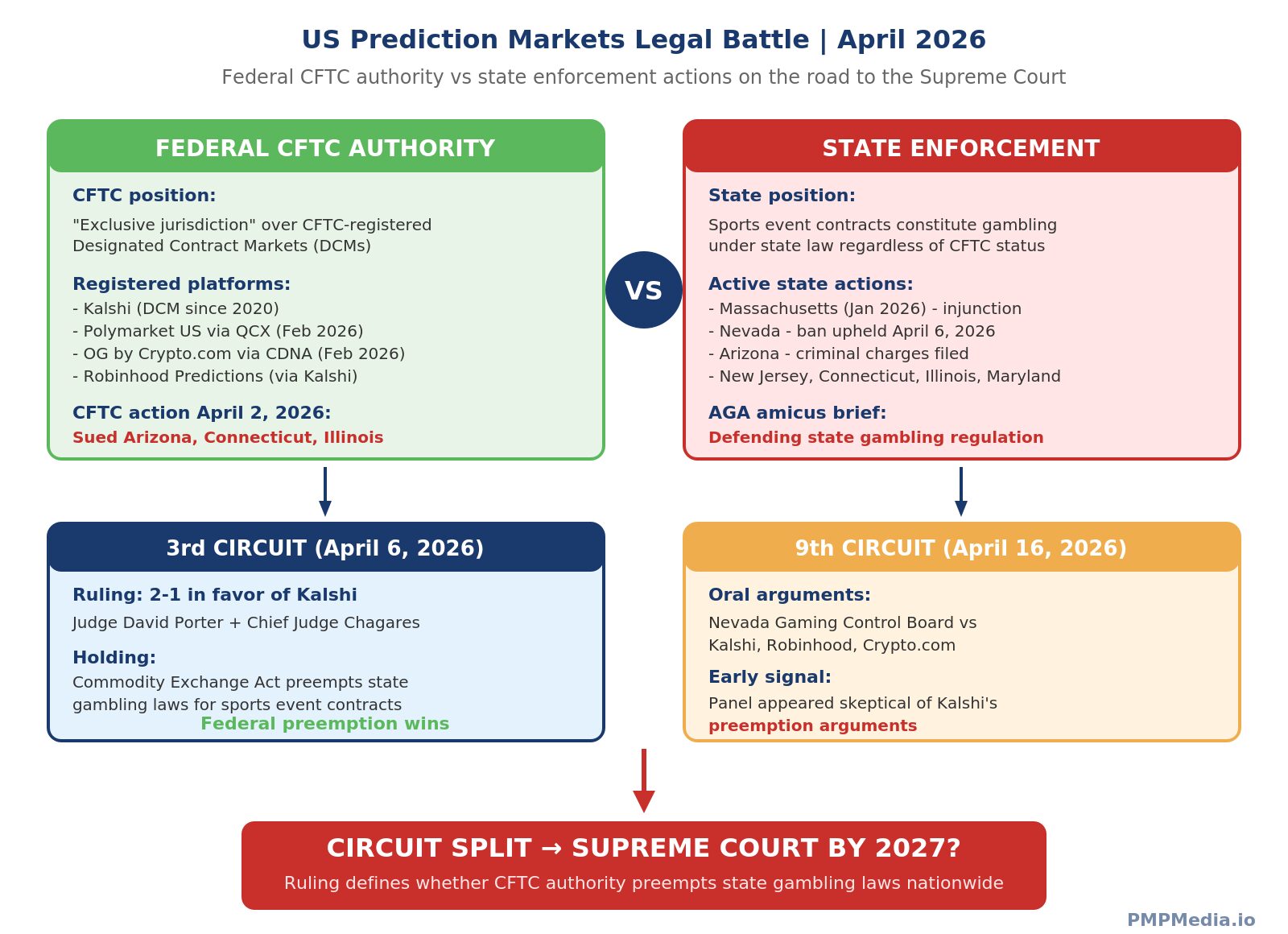

United States: Federal Authority vs State Enforcement

The US regulatory picture is the most consequential and the most complicated. Understanding it requires tracking three parallel tracks at once: federal CFTC authority, state-level enforcement actions, and federal court rulings on which one prevails.

The federal framework

Kalshi holds a Designated Contract Market license from the Commodity Futures Trading Commission, granted in 2020. That license lets Kalshi self-certify event contracts under the Commodity Exchange Act, with the CFTC retaining authority to review and prohibit contracts that fall under a specific “gaming” prohibition rule. Polymarket US operates through QCX, a CFTC-registered exchange Polymarket acquired in early 2026.

The CFTC under Chairman Michael Selig has taken an aggressive pro-prediction-markets stance. Selig has asserted the agency has “exclusive jurisdiction” over DCM-registered prediction markets, withdrew a 2024 proposal to ban event contracts, and rescinded a 2025 advisory warning firms about offering these products. On April 2, 2026, the CFTC took the unusual step of suing Arizona, Connecticut, and Illinois, arguing that the Commodity Exchange Act preempts those states’ gambling laws as applied to event contracts.

State enforcement actions

Multiple states have disagreed. They argue that sports event contracts constitute gambling under their state laws regardless of federal commodities registration, and they have taken enforcement action accordingly.

The most significant state actions as of April 2026 include:

- Massachusetts: First state to go on offense. In January 2026, a Suffolk County Superior Court judge issued a preliminary injunction barring Kalshi from offering sports contracts to in-state users without a gambling license

- Nevada: The Gaming Control Board sued Kalshi. A Nevada judge upheld the state’s ban on April 6, 2026, and ordered Kalshi to adopt geofencing by May 4

- New Jersey: State sued by Kalshi. A federal district court sided with Kalshi, finding the Commodity Exchange Act preempts state law. Third Circuit affirmed on April 6, 2026

- Maryland: State won. The District of Maryland denied Kalshi’s preliminary injunction, reasoning that the CEA does not encompass state gambling laws

- Arizona: Filed criminal charges against Kalshi in February 2026. A US District Judge allowed Arizona to press those charges in April 2026, despite the CFTC’s suit against the state

- Connecticut, Illinois: Targets of the CFTC’s April 2, 2026 federal lawsuits

- Washington State: AG Nick Brown publicly argued the case against prediction markets in April 2026

The Third Circuit ruling and the path to the Supreme Court

On April 6, 2026, the US Court of Appeals for the Third Circuit issued the first federal appellate ruling on this question, in KalshiEX LLC v. Flaherty. The 2-1 decision, authored by Judge David Porter and joined by Chief Judge Michael Chagares, held that the Commodity Exchange Act preempts state gambling laws as applied to sports-related event contracts on CFTC-registered DCMs.

The reasoning: Kalshi’s sports event contracts qualify as “swaps” under the CEA, and the CEA’s comprehensive regulatory framework for designated contract markets creates field preemption that overrides state gambling classification. Put more simply, if the CFTC has not determined a contract is contrary to public interest, state regulators cannot override that implicit approval.

Judge Patty Shwartz dissented, describing Kalshi’s products as “virtually indistinguishable from the betting products available on online sportsbooks” and arguing that the presumption against preemption should apply with “special force” in the field of gambling regulation.

The Ninth Circuit heard consolidated oral arguments on April 16, 2026, in cases involving Kalshi, Robinhood, and Crypto.com challenging the Nevada Gaming Control Board. Reports from the hearing suggested judges appeared skeptical of Kalshi’s preemption arguments. If the Ninth Circuit rules against Kalshi, the resulting circuit split would almost certainly produce a Supreme Court case by 2027 that would definitively resolve whether state gambling laws can be enforced against CFTC-registered event contracts.

Professional sports leagues enter the debate

In April 2026, the NFL formally requested that prediction market operators remove contracts the league considers “objectionable bets,” including player-performance props, injury-related markets, and contracts that could create incentives for game manipulation. The NBA and MLB have made similar requests. The American Gaming Association filed an amicus brief in the Third Circuit case arguing that federal preemption of state gambling laws would undermine a decade of careful state-by-state regulatory development.

This is not just policy theater. Sports leagues have spent years building integrity-monitoring frameworks with licensed sportsbook operators, including real-time data sharing and suspicious activity reporting. If prediction markets operate outside that framework at scale, the leagues lose visibility into betting markets tied to their events.

Political markets and federal policy

Political event contracts got clearer in 2024 when a federal court ruled in Kalshi’s favor against the CFTC, holding that election-based contracts did not constitute illegal gambling under the CEA. The CFTC initially appealed but dropped the appeal after the Trump administration change in May 2025. Since then, political markets have operated without significant regulatory challenge.

Representative Chris Murphy announced plans in 2026 to propose legislation regulating prediction markets, citing concerns that government officials might profit from inside knowledge on military-related contracts. The Public Integrity in Financial Prediction Markets Act would require residency proof for users exceeding specific thresholds. Neither bill has passed as of April 2026.

United Kingdom: Clear Gambling Framework

The UK has taken the opposite approach to the US and resolved the regulatory question clearly in favor of gambling classification.

The Gambling Commission issued guidance in February 2026 confirming that prediction markets fall within the Gambling Commission’s remit rather than the Financial Conduct Authority’s. The UKGC classifies prediction markets as a form of betting intermediary, analogous to existing betting exchanges like Betfair.

Under this framework, any operator serving UK users must hold a Gambling Commission license, comply with consumer protection requirements, meet anti-money laundering obligations, and operate under UK gambling tax rules. Operators themselves pay gambling tax. Player profits remain tax-free (consistent with general UK betting taxation). This approach explicitly excludes FCA authorization as the regulatory path.

The commercial implications are significant. Polymarket and Kalshi cannot legally serve UK users. Only UK-licensed operators can offer prediction markets in Britain. As of April 2026, two platforms have launched under this framework:

- Matchbook Predictions: Launched in January 2026, becoming the first UK-licensed prediction market. Operates under Matchbook’s existing UKGC exchange license, with initial focus on sports. The platform also provides a white-label product for easyBet, part of easyJet founder Stelios Haji-Ioannou’s business group. Matchbook is using the UK launch as a controlled road test for US expansion via its American partner RSBIX, which has filed for CFTC Designated Contract Market approval

- Betfair Predicts: Launched in April 2026 as an invite-only beta. Betfair Predicts operates effectively as a reskin of the existing Betfair Exchange product, classified as gambling under Betfair’s existing UKGC license. Staff at Betfair supported FanDuel in the US with technical expertise for FanDuel Predicts

The UK approach has one practical advantage. By treating prediction markets as betting intermediaries, the UK has avoided the federal-vs-state classification mess that is dominating US courts. The regulatory question was resolved in one regulator, with one framework, consistently applied.

European Union: Fragmented and Mostly Hostile

The EU has no unified regulatory framework for prediction markets. Gambling is regulated at the member state level rather than the EU level, which has produced a patchwork of national responses, overwhelmingly skeptical of the major platforms.

Countries that have explicitly banned or restricted prediction markets

As of March 2026, the following EU and adjacent jurisdictions have taken enforcement action against Polymarket, Kalshi, or both:

- France: The Autorité Nationale des Jeux (ANJ) issued a statement declaring prediction market platforms “are not authorised in France and are considered illegal gambling services,” citing addictive characteristics amplified by absence of protective mechanisms

- Germany: The Joint Gambling Authority of the German Federal States (GGL) warns against Polymarket as illegal under the Interstate Treaty on Gambling. Events must appear in an official programme to be legally bet on, which effectively excludes most prediction market questions

- Netherlands: The Kansspelautoriteit issued a penalty order against Polymarket ordering it to cease operations

- Belgium: Gaming Commission added Polymarket to its blacklist of illegal gambling websites

- Portugal: Banned Polymarket after uncovering suspicious trading during the January 2026 presidential election, when over €4 million was placed in a couple of hours before the result was announced, raising insider trading concerns

- Italy: Restricted Polymarket under gambling regulation

- Poland, Romania, Cyprus, Greece: All have blocked Polymarket under national gambling frameworks

- Switzerland: Restricted access under national gambling law

- Ukraine: The Commission for Regulation of Gambling and Lotteries (KRAIL) blocked Polymarket, partly due to unauthorised wagering on sensitive national military outcomes

The pattern is clear. Where EU and adjacent member states have taken a position, the default answer has been “this is gambling, it needs a local license, the platform does not have one, block it.”

Gibraltar: First EU-adjacent licensed platform

On March 26, 2026, Gibraltar became the first European jurisdiction to license a prediction market operator when it approved PredictStreet under its gambling framework. Gibraltar Minister for Justice Nigel Feetham described the process as “record-setting.” PredictStreet launched April 9, 2026, with a focus on FIFA World Cup 2026 markets, positioning itself as a licensed European alternative to Polymarket in jurisdictions where Polymarket is blocked.

Gibraltar’s move matters because it demonstrates that an EU-adjacent regulator can build a framework to license prediction markets rather than simply banning them. Malta has signaled interest in developing its own framework but moved more slowly.

The MiFID II question

The theoretical alternative to gambling regulation in the EU would be classifying prediction market contracts as financial instruments under MiFID II. This would place them under securities regulation with rules around market integrity, disclosure, and licensing of investment firms.

MiFID II does not provide an exhaustive definition of financial instruments but enumerates options, futures, swaps, forwards, contracts for differences, credit derivatives, and certain commodity contracts in Annex I Section C. Prediction market contracts whose underlying events are linked to financial or economic outcomes (interest rates, equity prices, commodity values) could plausibly fall under MiFID II as derivatives. Contracts on non-financial events like elections, sports, or cultural outcomes do not fit as cleanly.

No EU member state has formally adopted a MiFID II-based approach to prediction markets as of April 2026. Academic and legal commentary (particularly from Oxford Business Law Blog and firms like Taylor Wessing) suggests this is the likely long-term direction for financially-themed prediction markets, while event-based markets remain under gambling law. Practitioners expect this distinction to formalise over 2026-2027.

MiCA and crypto-based platforms

The EU’s Markets in Crypto-Assets (MiCA) regulation comes into full effect in July 2026, with the grandfathering period for securing a Crypto-Asset Service Provider licence ending at that point. Since Polymarket and similar platforms use cryptocurrency (USDC on Polygon for Polymarket), MiCA applies to their operations in EU member states. The European Securities and Markets Authority has confirmed MiCA’s strict market abuse regimes apply to prediction markets using crypto assets.

This creates another compliance layer on top of existing gambling restrictions. A prediction market operating in an EU member state would need both gambling authorisation (at the member state level) and MiCA compliance (at the EU level) if it uses crypto settlement.

Australia and New Zealand: Explicit Gambling Bans

Both Australia and New Zealand have taken firm positions classifying prediction markets as illegal gambling.

Australia: The Australian Communications and Media Authority (ACMA) determined in August 2025 that Polymarket constituted a “prohibited and unlicensed regulated interactive gambling service” under the Interactive Gambling Act 2001. ACMA directed internet service providers to block access to Polymarket domains and APIs. The trigger was a Crikey investigation that revealed Polymarket had paid Instagram and TikTok influencers to promote its Australian federal election markets. Between November 2024 and May 2025, Australians recorded over 1.88 million visits to Polymarket despite the platform’s nominal geoblocking.

ACMA’s reasoning explicitly rejected the financial instrument framing: “Australian users were not engaging with Polymarket to make financial decisions as defined under national law. Instead, the platform’s markets are better classified under gambling legislation.”

New Zealand: The Department of Internal Affairs ruled in February 2026 that prediction markets like Polymarket and Kalshi are prohibited under the Gambling Act 2003 and the Racing Industry Act 2020. The ruling came alongside New Zealand’s progress on the Online Casino Gambling Bill, which auctions 15 online casino licenses. TAB holds a monopoly over online sports betting in New Zealand, and prediction markets compete directly with that monopoly, which partly motivated the hard-line regulatory position.

Unlike Australia, New Zealand does not currently geoblock gambling websites. Polymarket and Kalshi remain accessible to New Zealand users unless the platforms independently block access.

Canada: Fragmented Provincial Approach

Canada regulates gambling at the provincial level, which has produced a patchwork similar to but smaller than the US state-level situation.

Ontario: The most restrictive province. Polymarket’s operations in Ontario have been limited following regulatory settlements. Kalshi restricts all Canadian users as a general policy. No major international prediction market operates openly in Ontario.

Other provinces have mixed enforcement positions. Quebec, British Columbia, and Alberta have not taken formal action against Polymarket specifically, but their regulatory frameworks treat unlicensed online gambling generally as illegal. This leaves international prediction markets in a grey area where they are technically not permitted but also not actively enforced against.

No Canadian-licensed prediction market operates at national scale as of April 2026.

Asia: Mostly Restrictive

Singapore: Maintains strict prohibitions on unlicensed remote gambling under the Remote Gambling Act. Prediction markets fall under this ban by default. Polymarket explicitly restricts Singapore users.

Taiwan, Thailand: Geoblocked by Polymarket, reflecting their strict anti-gambling regulatory postures.

Japan, South Korea, India: Not explicitly banned. Polymarket operates in these markets. Tokyo and Seoul have active retail prediction market participation. No local licensing framework exists, which means platforms operate without formal authorisation but also without active enforcement.

China: Both Polymarket and Kalshi are inaccessible without VPN circumvention. Polymarket has quietly begun targeting Chinese users despite the country’s strict gambling laws, hiring Mandarin speakers and listing bets tied to the Lunar New Year. Asia monthly trading volume on Polymarket reportedly reaches hundreds of millions of dollars.

Latin America: Mostly Open, With Exceptions

Latin America has been more permissive than other regions, with significant exceptions.

Brazil: Regulators have not established whether prediction markets fall under the Securities Commission (CVM) or the Ministry of Finance’s Secretariat of Prizes and Betting. Polymarket operates openly in Brazil as of April 2026, with Brazil being one of the platform’s most active markets by volume.

Argentina: Previously open, but a Buenos Aires judge banned Polymarket nationwide in March 2026, declaring it an unlicensed betting platform. The ruling deemed Polymarket an unauthorised gambling operator under Argentine law.

Chile: No formal restrictions. Polymarket maintains active user base.

Mexico: No explicit action against prediction markets. Operates in a regulatory grey area.

Prediction Markets Regulation vs Gambling Regulation

Understanding why the classification question matters requires understanding what each regulatory framework actually does.

Gambling regulation framework

Gambling regulation focuses on consumer-facing risks: problem gambling, underage access, fairness of games, integrity of competitions. Standard components include:

- Per-operator licensing with significant capital requirements and ongoing compliance obligations

- Mandatory responsible gambling controls (deposit limits, self-exclusion, reality checks)

- Advertising restrictions to protect minors and vulnerable populations

- Anti-money laundering and source-of-funds requirements

- Integrity monitoring through data sharing with sports leagues and integrity bodies

- Per-jurisdiction licensing (state in US, province in Canada, national in most EU states)

- Tax structures that capture a percentage of gross gaming revenue

Financial regulation framework

Financial regulation focuses on market integrity, investor protection, and systemic risk. Standard components include:

- Registration of trading venues as exchanges, ATSs, or DCMs

- Market surveillance and trade reporting

- Insider trading and market manipulation prohibitions (enforced criminally)

- Capital requirements and clearing infrastructure

- Investor disclosure requirements

- Federal or supranational authority (one set of rules, not 50)

- Tax structures that capture income on realised gains

The practical difference

For operators, the difference is operational. A financial-instrument classification means one federal license, uniform rules, standard securities-industry infrastructure. A gambling classification means 50 state licenses (or equivalent), different rules in each jurisdiction, gambling-specific compliance infrastructure. The federal path is significantly cheaper and easier to scale.

For users, the difference is consumer protection. Gambling frameworks include explicit responsible gambling tools. Financial frameworks do not. If a prediction market operates under CFTC authority, the responsible gambling tools that sportsbooks must offer are not required.

For state regulators, the difference is revenue and control. State gambling taxes capture a meaningful share of gross revenue. Federal commodities classification means states collect nothing, and lose the policy levers they have built over a decade of legalised sports betting. This is why state attorneys general are fighting this hard.

For a deeper look at this structural comparison, see our prediction markets vs betting analysis.

Current Regulatory Flashpoints

Sports contracts: the most contested category

Understanding prediction markets regulation requires understanding where they fit in the broader gambling license landscape. Different jurisdictions classify them under different license categories: US as CFTC Designated Contract Market, UK as betting intermediary under UKGC, EU member states mostly as gambling requiring local licensing.

Sports event contracts are the specific category driving most of the US legal battles. Political contracts have relative federal clarity after Kalshi’s 2024 court victory. Sports contracts do not.

The reason: sports betting is a $17 billion US industry with decade of state-level regulatory development. If prediction markets can legally offer contracts on the same sporting events that state-licensed sportsbooks cover, they undercut that entire ecosystem. A bettor paying state gaming tax on a $100 NFL bet through DraftKings would see no reason to pay the same tax on an identical Kalshi contract with no state oversight.

Kalshi’s March 2026 volume was $12.35 billion, with 87% coming from sports contracts. This is not a marginal policy debate. It is a direct competitive threat to state-regulated sportsbooks, and it is why Nevada, New Jersey, Massachusetts, Arizona, Connecticut, Illinois, and Maryland have all engaged.

Insider trading on prediction markets

Portugal’s January 2026 investigation into presidential election trading (€4 million placed in hours before the announcement) highlights a regulatory gap. If prediction markets are classified as gambling, insider trading rules from financial markets law do not apply. If they are classified as financial instruments, they should, but enforcement is difficult across jurisdictions and user bases.

The broader question is whether classical insider trading frameworks translate to prediction markets. EU’s Market Abuse Regulation applies to instruments traded on regulated markets, but prediction market contracts on events like elections are not traditionally “instruments” in that regulatory sense. This gap is likely to tighten through 2026-2027 as enforcement actions accumulate.

Manipulation risks at scale

Ceasefire predictions in April 2026 sparked concerns about Polymarket insider trading when large positions were placed on specific diplomatic outcomes shortly before public announcements. The NFL has specifically flagged prop bet contracts as susceptible to manipulation: a single player’s performance is easier to manipulate than a team outcome, and the financial incentives on event contracts can be large enough to justify manipulation attempts.

Both Polymarket and Kalshi have integrity monitoring programmes, but they operate outside the traditional sports integrity framework built with licensed sportsbooks. This gap is a major argument used by state regulators and sports leagues arguing for gambling-style regulation.

Global Trends to Watch Through 2027

US Supreme Court resolution

The Third Circuit and Ninth Circuit rulings have set up a circuit split on federal preemption. If the Ninth Circuit rules against Kalshi (as expected based on April 16 oral argument reports), the Supreme Court will almost certainly take the case. Resolution is likely in the 2027 term. The outcome will define whether sports event contracts are federal-only or state-regulable, and whether the CFTC’s “exclusive jurisdiction” claim survives Constitutional review.

Either outcome is consequential. A pro-CFTC ruling cements the federal framework and opens prediction markets to nationwide expansion. A pro-state ruling forces prediction markets to comply with state gambling laws, essentially requiring them to become sportsbooks with state licenses.

Institutional adoption drives regulatory clarity

Media partnerships (Kalshi-Fox Corporation in April 2026, CNN and CNBC integrating Kalshi data into broadcasts, DAZN-Polymarket) and institutional interest (CME Group CEO Terrence Duffy describing prediction markets as “a legitimate domain of speculation and information aggregation that our clients are demanding”) create pressure for regulatory certainty. Institutions do not deploy capital into contested legal frameworks. As prediction markets become embedded in financial news and institutional data feeds, the pressure for clear federal-level regulation will intensify.

European convergence around gambling classification

EU member states have overwhelmingly treated prediction markets as gambling. As more member states take formal positions, informal convergence around this classification is likely. A future EU-level initiative (similar to MiCA for crypto assets) could formalise this through coordinated gambling regulation or an explicit MiFID II carve-in for financial-themed event contracts.

UK model as export template

The UK’s clear Gambling Commission framework has avoided most of the problems bedeviling the US. Common Law jurisdictions following UK regulatory traditions (Australia, New Zealand, South Africa, Ireland, Singapore) are more likely to adopt the UK approach than the US approach. This could produce a durable split between the CFTC-led US model and a UK-led gambling model across the Commonwealth and adjacent markets.

Market structure evolution

Regulatory pressure is accelerating consolidation. Smaller decentralized platforms face mounting compliance costs they cannot absorb. Institutional-backed platforms (Kalshi with Series E at $22B valuation, Polymarket following similar trajectory) have the resources to litigate and lobby. The prediction markets of 2028 will likely be dominated by a handful of heavily-capitalised, federally-regulated US platforms plus regionally-licensed alternatives in the UK, Gibraltar, Malta, and emerging frameworks in other jurisdictions.

What This Means for Operators and Investors

The regulatory landscape creates a clear strategic calculus.

For US-focused operators: CFTC DCM registration remains the gold standard. The Third Circuit ruling dramatically strengthens the legal position, but state-level risk remains until the Supreme Court rules. Operators without CFTC registration face existential legal risk. Sleeper Markets LLC sued the CFTC in late 2025 alleging the agency was intentionally delaying its DCM application, which underscores how much the license matters.

For globally-focused operators: Jurisdiction strategy matters more than product design. Operating in 160+ countries simultaneously (Polymarket model) means accepting blocks in restrictive jurisdictions and running compliance costs for diverse legal regimes. Operating in a single gambling-licensed jurisdiction (Matchbook UK model) is cleaner but smaller.

For investors: The CFTC’s pro-prediction-markets stance under Selig is not permanent. A change of administration or a regulatory personnel change could reverse the current enforcement posture. Capital deployed on the assumption that federal preemption holds is taking Supreme Court risk. Capital deployed into gambling-licensed platforms in specific jurisdictions takes less regulatory risk but accepts smaller market size.

For institutional users: Risk management and compliance workflows are more complex for prediction markets than for traditional derivatives. Firm policies around employee trading, insider trading, and disclosure need to contemplate event contracts specifically. The regulatory uncertainty also creates operational risk that traditional derivatives do not have.

Related Guides

- Prediction Markets Guide

- What Are Prediction Markets

- Are Prediction Markets Legal

- Prediction Markets vs Betting

- Best Prediction Markets Platforms

- Polymarket Review

- Kalshi Review

- Global iGaming Regulation Guide

The Bottom Line

Prediction markets regulation in 2026 is genuinely unsettled, and the next 12-18 months will resolve some of the biggest open questions. The US Supreme Court is the most consequential variable. A ruling confirming CFTC exclusive jurisdiction unlocks nationwide expansion and validates the federal framework. A ruling against federal preemption forces prediction markets to become state-licensed sportsbooks, which would collapse the competitive advantage they currently hold.

Outside the US, the picture is more settled but less favourable. The UK has a working gambling framework. Most of the EU has explicit bans. Australia and New Zealand have blocked access. Asia is mostly restricted. Latin America is mostly open with Argentina as a recent exception. That pattern is unlikely to shift dramatically absent a coordinated international framework, which nothing in 2026 suggests is coming.

For anyone participating in this market (as operator, investor, or user), the regulatory layer is now as important as the product itself. The winners will be platforms that can navigate multiple regulatory frameworks at once, maintain compliance costs as a core infrastructure investment, and litigate effectively when challenged. The losers will be platforms that assume either regulatory framework will win cleanly. Neither is going to.

FAQ

Are prediction markets legal in the US?

Yes, at the federal level. Kalshi holds a CFTC Designated Contract Market license, and Polymarket US operates through the CFTC-registered QCX exchange. Sports contracts face active state-level legal challenges in Massachusetts, Nevada, Arizona, Connecticut, Illinois, and Maryland. The Third Circuit ruled in favor of federal preemption on April 6, 2026. The Ninth Circuit is expected to rule differently, which would set up a Supreme Court case by 2027.

Who regulates prediction markets in the UK?

The UK Gambling Commission. Prediction markets are classified as betting intermediaries, analogous to existing betting exchanges like Betfair. The Financial Conduct Authority does not have regulatory jurisdiction. Only UK Gambling Commission-licensed operators (Matchbook Predictions since January 2026, Betfair Predicts since April 2026) can legally serve UK users.

Why are Polymarket and Kalshi blocked in the EU?

Most EU member states classify prediction markets as gambling under national gambling laws and block platforms that do not hold local licenses. France (ANJ), Germany (GGL), Netherlands (Kansspelautoriteit), Belgium, Portugal, Italy, Poland, Romania, Cyprus, Greece, and others have taken this position. The EU has no unified prediction markets framework because gambling is regulated at the national level.

Can prediction markets operate under MiFID II?

Potentially for financially-themed event contracts, but not yet in practice. MiFID II’s Annex I Section C enumerates derivatives including options, futures, swaps, and forwards. Financially-linked prediction contracts (rates, commodities, equities) could plausibly fit. Event-based contracts (elections, sports, culture) fit less cleanly. No EU member state has formally adopted a MiFID II approach to prediction markets as of April 2026.

What happens if the Supreme Court rules against Kalshi?

A Supreme Court ruling that state gambling laws can be enforced against CFTC-registered event contracts would force Kalshi, Polymarket US, and other platforms to comply with state gambling frameworks. This would effectively require them to become state-licensed sportsbooks for sports contracts, with per-state licensing costs and state-specific rules. The federal competitive advantage would collapse.

Are prediction markets legal in Canada?

Limited. Ontario restricts Polymarket and Kalshi restricts all Canadian users. Other provinces have mixed enforcement. No Canadian-licensed prediction market operates at scale. The practical answer for Canadian users is access through VPN or not at all.

How does the CFTC approve or prohibit event contracts?

Under the CFTC Prohibition Rule (Rule 40.11), CFTC-registered DCMs can self-certify that contracts comply with the Commodity Exchange Act. The CFTC can review and prohibit contracts contrary to public interest, including gaming-related contracts. The agency’s interpretation of what constitutes “gaming” is itself contested, which is how sports contracts ended up in federal court.

What about political event contracts?

Relatively clear federally. A 2024 federal court ruling in Kalshi’s favor held that election-based contracts did not constitute illegal gambling under the CEA. The CFTC dropped its appeal in May 2025 under the Trump administration. Political markets have operated without significant regulatory challenge since. Representative Chris Murphy has proposed legislation to regulate political prediction markets over insider trading concerns, but no bill has passed.

Do prediction markets need anti-money laundering controls?

Yes, typically. CFTC-registered DCMs must comply with Bank Secrecy Act and anti-money laundering requirements. UK-licensed operators comply with UKGC AML rules. EU-blocked operators face MiCA compliance for crypto-based products. Offshore unlicensed operators face AML requirements informally through banking relationships but may not comply rigorously. This is a growing enforcement area.

What is the MiCA impact on prediction markets?

The EU’s Markets in Crypto-Assets regulation comes into full effect in July 2026. Prediction market platforms using cryptocurrency (Polymarket’s USDC on Polygon) are subject to MiCA’s market abuse regimes and Crypto-Asset Service Provider licensing requirements when operating in EU member states. This adds compliance overhead on top of existing gambling restrictions in member states that have blocked access.

Which countries allow Polymarket today?

Brazil, Chile, India, Japan, South Korea, Switzerland, Spain, Greece, New Zealand (despite formal illegality), and approximately 160 other countries where enforcement is not active. Polymarket geoblocks approximately 33 jurisdictions including Australia, Belgium, Germany, France, UK, Italy, Netherlands, Poland, Portugal, Romania, Singapore, Taiwan, Ukraine, United States, and Argentina (added March 2026).

Is Gibraltar licensing significant?

Yes, as a regulatory signal. Gibraltar became the first European jurisdiction to license a prediction market operator (PredictStreet) on March 26, 2026. This demonstrates that European-adjacent regulators can build prediction markets frameworks rather than defaulting to bans. Malta has signaled interest in following. This creates a path for licensed European alternatives to Polymarket in jurisdictions where Polymarket is blocked.

Share

Share

0 views

0 views

Analysis

Analysis  Business

Business  Companies

Companies  Crime

Crime  Finance

Finance  M&A

M&A  Prediction Markets

Prediction Markets  Regulation

Regulation  Reports

Reports