Kalshi went from legal underdog to $22 billion prediction market powerhouse in about 14 months, and the old framing of “Kalshi is the quieter, more structured alternative to Polymarket” no longer describes what is actually happening on the platform. In March 2026, Kalshi processed $12.35 billion in trading volume, the highest of any prediction market globally. Weekly volumes routinely exceed $2 billion during major sports events. The company closed a $1 billion Series E at an $11 billion valuation in December 2025, then doubled that to $22 billion in a March 2026 round led by the same core investors.

That is not a quiet platform with stable, predictable prices. That is the fastest-growing financial exchange in the United States.

This review covers Kalshi as it actually operates in April 2026: the CFTC-regulated structure, the real fee formula (not the vague descriptions that show up in most reviews), the ongoing state-by-state legal war over sports contracts, and the practical trade-offs versus Polymarket for users deciding where to put capital.

I will give you the bottom line first, because a lot of people reading this want the answer before the deep dive: Kalshi is the best prediction market for US-based users in 2026, period. The regulatory certainty, fiat onboarding, FDIC insurance, and sports liquidity are not matched by any competitor available to Americans. The weakness is fees, which are meaningfully higher than Polymarket International on most markets, and the real risk is that the state lawsuits eventually force Kalshi to exit sports in more jurisdictions than just Massachusetts.

Quick Verdict

Kalshi works for US users who want a legitimate, regulated prediction market with full fiat deposits and serious liquidity on sports, politics, and macro. It is less compelling for non-US users who have access to Polymarket International, and it is less attractive for active traders who are highly fee-sensitive. For most American retail users who are not already deep in crypto, Kalshi is the default answer.

Kalshi is fundamentally a US product. Non-US users have limited access and generally benefit more from alternatives. UK users in particular have a growing set of prediction market options operating under UK Gambling Commission licensing rather than CFTC — Matchbook Predictions launched January 2026 as the first UKGC-licensed prediction market, and Betfair Predicts followed in April 2026.

What Kalshi Is in 2026

Kalshi is the largest federally regulated prediction market in the United States, operating as a Designated Contract Market under the Commodity Futures Trading Commission. The company was founded in 2018 and spent years fighting the CFTC for the right to list political event contracts, finally winning that case in 2024 and opening the floodgates for everything that followed.

The trading model is straightforward: binary contracts priced between $0.01 and $0.99 that pay $1.00 if the event occurs and $0 if it does not. Users trade against each other through a central limit order book, and Kalshi charges fees on taker orders while offering maker rebates on some markets. The economic model is closer to CME than to a sportsbook, which is exactly the positioning Kalshi has leaned into.

What makes Kalshi different from every other prediction market is federal regulatory legitimacy. Balances are FDIC-insured up to $250,000. The exchange runs standard derivatives market infrastructure. Institutional traders can onboard through prime brokerage relationships. None of this exists at Polymarket, which is why institutional capital has flowed almost exclusively into Kalshi rather than its offshore competitors.

WHAT THIS ACTUALLY MEANS

The “regulated vs unregulated” framing in most Kalshi reviews is too abstract. In practical terms, regulation means: your deposits are protected if Kalshi fails, the exchange cannot rug-pull your positions, disputes have a clear legal path through the CFTC, and institutional capital can participate without compliance teams blocking the activity. For users trading $1,000 positions, this matters less. For anyone trading at scale, it is the only thing that matters.

Volume, Valuation and Growth

The numbers behind Kalshi in 2026 are the story the old review completely missed. Here is what the platform actually looks like from a business perspective:

- March 2026 trading volume: $12.35 billion (the highest in prediction market history)

- 2025 annual volume: $23.8 billion, up 1,100% year-over-year

- Weekly volume during peak events: Consistently above $2 billion

- Series E valuation (December 2025): $11 billion, led by Paradigm with Sequoia, a16z, CapitalG, and ARK Invest participating

- Latest valuation (March 2026): $22 billion after a $1 billion follow-on round

- Active markets: 3,500+ across sports, politics, economics, weather, entertainment, and crypto

- Sports share of volume (March 2026): 87%, driven by NCAA March Madness basketball

Sports event contracts have been the dominant growth driver since Kalshi rolled them out nationally in January 2025. Before that rollout, the platform was doing a few hundred million a month in volume, mostly politics and economics. Sports took Kalshi from prediction market curiosity to legitimate competitor to DraftKings and FanDuel within a single year. That is also why Kalshi is now the target of state-level lawsuits.

How Kalshi Fees Actually Work

The standard review complaint about Kalshi is that fees are opaque. They are not. The formula is publicly documented and has been stable for years. What is opaque is how the formula behaves in practice, which is what most reviews fail to explain.

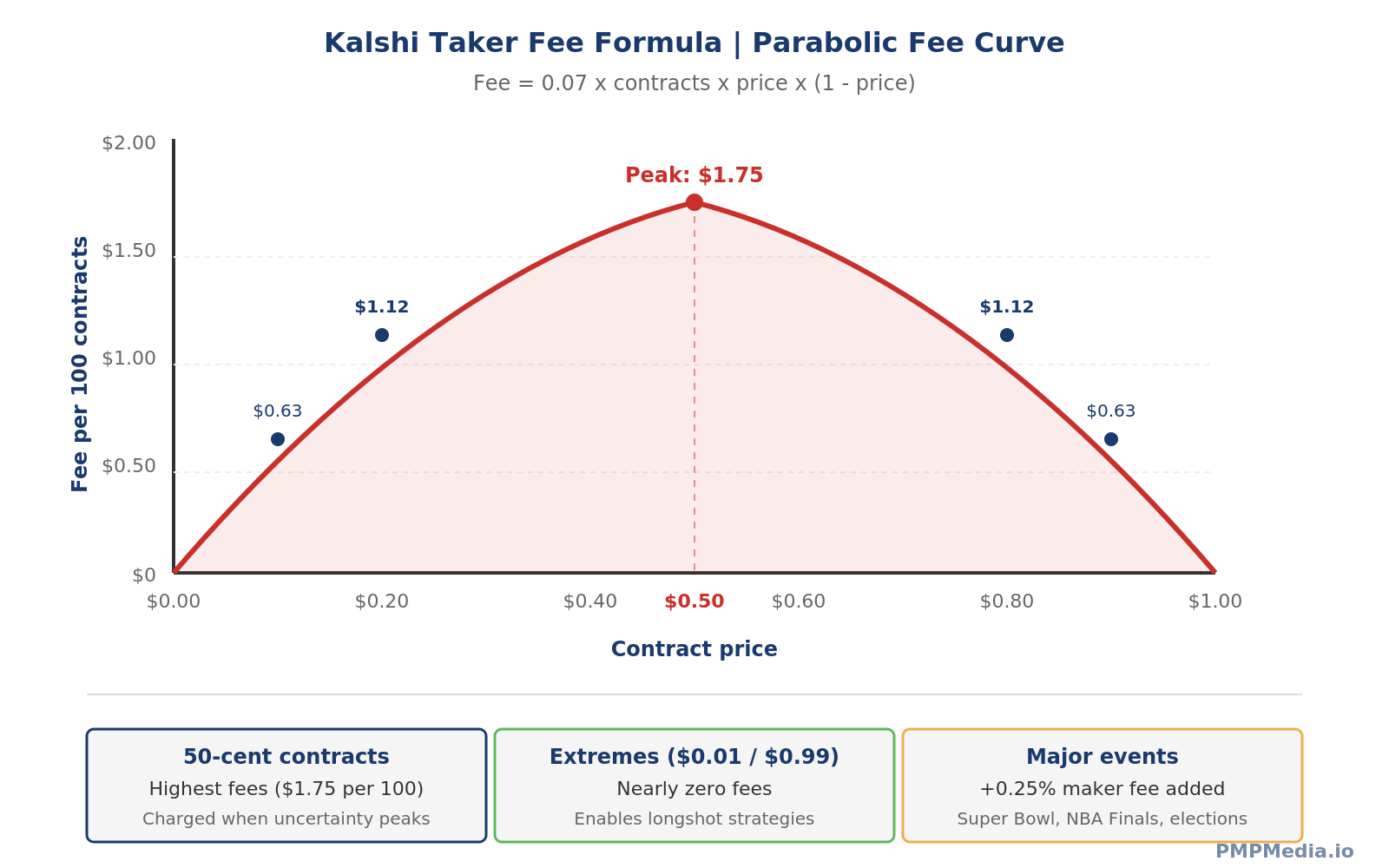

The Taker Fee Formula

Kalshi’s taker fee is calculated as:

Fee = 0.07 × contracts × price × (1 − price)

This produces a parabolic curve. Fees are highest when contracts trade near $0.50 (maximum uncertainty, $1.75 per 100 contracts) and approach zero at the extremes. At a $0.99 contract, the fee is basically nothing. At a $0.80 contract, it is $1.12 per 100. At $0.50, it peaks at $1.75 per 100 contracts.

This structure makes sense once you understand what it is optimising for. Charging flat fees would make extreme-probability contracts ($0.02 longshots, $0.98 favourites) prohibitively expensive because the fee would consume a large fraction of the contract price. The parabolic curve solves this elegantly by scaling fees with market uncertainty rather than contract price.

The practical effect: Kalshi fees on typical contested markets (50/50 politics, sports point spreads) are meaningfully higher than Polymarket International in fee-enabled categories and dramatically higher than Polymarket’s fee-free categories like geopolitics. Kalshi peak fees are roughly 1.75%, while Polymarket peak fees range from 0% (geopolitics) to 1.80% (crypto), depending on category.

Maker Fees and Rebates

Standard Kalshi markets have a 0% maker fee, which is how liquidity providers make the economics work. During major events like the Super Bowl, NFL championships, NBA Finals, and presidential elections, Kalshi adds a 0.25% maker fee per contract. This is where the fee structure starts to hurt: on longshot contracts priced below 5 cents during major events, the 0.25% maker fee can represent 12-50% of the contract price, making extreme-probability strategies uneconomic.

Kalshi also runs a market maker rebate program with tiered rewards up to 1%, capped at $7,000 weekly. This is functional for serious liquidity providers but not useful for typical retail users.

The Idle Cash Advantage

Here is something that rarely shows up in reviews but actually matters: Kalshi pays 3.75-4.05% APY on idle account balances. For a trader holding $10,000 on the platform, that is roughly $400 per year in free money. Polymarket does not pay interest on idle USDC. Over a year, the APY substantially offsets Kalshi’s fee disadvantage for users who do not trade at extreme frequency. I have not seen this calculated properly in any other review I have read, but it changes the fee comparison meaningfully.

Deposit and Withdrawal Costs

- ACH bank transfer: Free (both deposit and withdrawal)

- Wire transfer: Free deposit, small fee on withdrawal

- Debit card: 2% processing fee (avoid)

- Apple Pay: Free, but requires small amounts

- Crypto (via ZeroHash partnership): Free, converted to USD on arrival

ACH is the default for most users. Debit card deposits should be avoided for anything other than tiny test amounts because the 2% processing fee is genuinely expensive compared to waiting a day for ACH to clear.

The Massachusetts Injunction and the State-by-State War

This is the single most important development in Kalshi’s 2026 story and the one most reviews either ignore or handle poorly. I will be direct about what is actually happening.

On January 20, 2026, a Suffolk County Superior Court judge issued a preliminary injunction barring Kalshi from offering sports event contracts to Massachusetts residents without a state gaming license. The injunction took effect in February 2026 after Kalshi’s emergency motion to stay was denied. This is the first state-level ban on Kalshi’s sports products to actually take effect.

The legal theory matters. Kalshi’s position is that the Commodity Exchange Act gives the CFTC exclusive jurisdiction over derivatives, including event contracts, which preempts state gaming laws. The Massachusetts court rejected this argument as “overly broad,” ruling that the CEA did not clearly demonstrate Congressional intent to displace state authority over gambling. Maryland had already ruled similarly in 2025, and Nevada dissolved its earlier injunction in favour of Kalshi in November 2025.

As of April 2026, Kalshi is in active litigation with multiple states:

- Massachusetts: Sports contracts banned for MA residents (injunction in effect)

- Nevada: Injunction dissolved, case ongoing

- Maryland: Lost motion for injunctive relief, appealed to Fourth Circuit

- Tennessee: Temporary restraining order in Kalshi’s favour, case continuing

- Ohio, Connecticut, New York: State enforcement paused by federal courts, preliminary motions pending

- Amicus brief from 38 states + DC: Filed in Maryland case arguing Kalshi’s sports contracts are “functionally indistinguishable” from sports wagering

WHAT THIS MEANS FOR USERS

If you are in Massachusetts, you cannot currently use Kalshi for sports contracts. Politics, economics, and other markets remain available. If you are in another state, the legal situation is uncertain but the products are currently available. The practical risk is that Kalshi could lose in another major state (California, New York, and Illinois are the biggest concerns) and be forced to geofence sports contracts in jurisdictions representing a meaningful share of US population. The company has $22 billion in backing to fight this, but the outcome is genuinely uncertain.

Kalshi vs Polymarket: Where Each Wins

I covered this comparison in detail in the Polymarket review, but from Kalshi’s side the trade-offs look slightly different. Here is the honest version for US users deciding between the two:

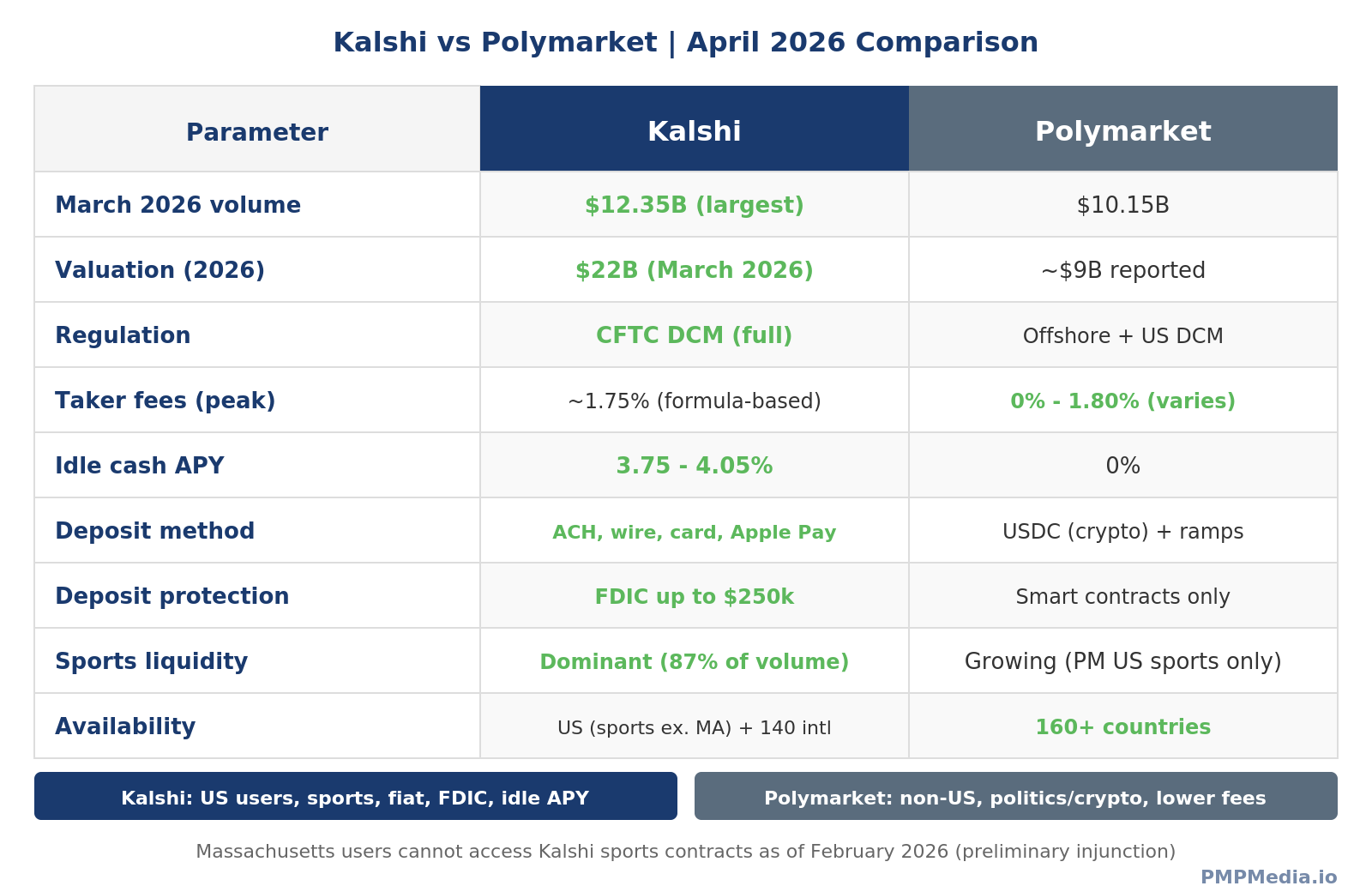

Where Kalshi Wins

- Regulatory protection: CFTC oversight, FDIC insurance up to $250,000, clear legal framework

- Fiat onboarding: ACH, wire, debit card, Apple Pay, no crypto required

- Sports liquidity: 2.5x Polymarket’s sports volume as of March 2026

- Idle cash APY: 3.75-4.05% on balances, which Polymarket does not pay

- Institutional access: The only US prediction market with real institutional capital

- Brokerage integration: Available through Robinhood (via Susquehanna joint venture), Coinbase, and others

- Media presence: Live odds integrated with CNN, CNBC, and other major news networks

Where Polymarket Wins

- Fees on most markets: Polymarket International has fee-free categories (geopolitics) and lower fees in most fee-enabled categories

- Global availability: 160+ countries vs Kalshi’s US-focused product plus 140 international countries

- No KYC on international platform: 2-minute signup vs Kalshi’s full KYC flow

- Politics and crypto liquidity: Deeper order books on global political and crypto narratives

- On-chain transparency: Every trade and settlement publicly verifiable

- No state-level litigation risk: Operating offshore means no US state can shut it down

My honest recommendation

For US users who are not already comfortable with crypto and who want full regulatory protection, start with Kalshi. The fee disadvantage is real but typically offset by the idle cash APY for moderate-frequency traders. The sports liquidity is better, the deposit infrastructure is smoother, and if something goes wrong, there is actually someone to complain to.

For non-US users, Polymarket International is almost always the better choice. There is no scenario where Kalshi offers a compelling advantage over Polymarket for someone in London, Tokyo, or São Paulo. The one exception is if you specifically want US sports and happen to find Kalshi’s international product easier to use, which happens occasionally but is not the default case.

User Experience in 2026

Kalshi’s app and website have improved substantially over the last 18 months. The early criticism that it felt like a trading terminal for finance professionals has been mostly addressed. Onboarding now takes 5-10 minutes including KYC. Deposits through ACH arrive within 1-2 business days. The mobile app is polished and supports all major features including limit orders, live order book, position management, and push notifications for market events.

What works well

- Interface is clean and learnable within 30 minutes

- Order book depth is clearly displayed on major markets

- Search and category navigation is functional

- Live market data updates without lag

- Sub-10ms execution for institutional VIP users

- Mobile app has feature parity with desktop

What still frustrates users

- KYC process is thorough but can catch out users with non-standard ID situations

- Some sports contracts have confusing resolution criteria that feel more like legal documents than sportsbook rules

- Position limits on political contracts ($100K per CFTC rules) can be restrictive for large traders

- The interface is optimised for traders who think in probabilities, which takes time for casual users

Available Markets

Kalshi offers more than 3,500 active markets at any given time, covering the following categories:

- Sports: NFL, NBA, MLB, NHL, NCAA football and basketball, golf, tennis, F1, soccer, UFC, boxing, and more. Moneyline, spread, over/under, and player prop contracts. This is the biggest category by volume.

- Economics: CPI releases, PPI, unemployment, GDP, Federal Reserve rate decisions, consumer sentiment. Macro hedging is genuinely useful here.

- Politics: Elections at federal and state level, congressional actions, policy outcomes. Position limits of $100K apply per CFTC rules.

- Weather: Temperature, hurricane, precipitation, and specialty weather contracts. Used by insurance and agriculture for hedging.

- Crypto: Bitcoin price targets, Ethereum milestones, adoption metrics. Less liquid than Polymarket crypto markets.

- Culture and entertainment: Oscars, Grammys, music chart positions, TV and film outcomes.

- Business and tech: IPO timelines, product launches, corporate earnings, AI benchmarks.

Who Kalshi Is Best For

- US residents outside Massachusetts who want regulated prediction market exposure

- Active sports traders looking for deep liquidity on American leagues

- Users who want to hedge real-world exposure (weather, macro, political)

- Institutional capital and professional traders who need regulatory clarity

- Users who value FDIC-insured balances and earning APY on idle cash

- Anyone uncomfortable with crypto wallets and USDC workflows

Who Should Think Twice

- Massachusetts residents who primarily want sports contracts

- Non-US users who have access to Polymarket International

- Highly fee-sensitive active traders making hundreds of trades per month

- Users whose main interest is political or crypto markets that Polymarket covers more deeply

- Traders who want anonymity (Kalshi requires full KYC)

Common Mistakes New Users Make

I have watched enough new traders learn Kalshi to see the patterns clearly. These are worth flagging because they cost people real money.

Treating 50-cent contracts as if fees do not matter. Fees peak at $0.50 and are substantially higher than on extreme-probability contracts. If you are trading coin-flip markets at high frequency, the fees compound quickly.

Using debit card deposits. The 2% processing fee on debit card deposits and withdrawals is genuinely expensive. ACH is free and takes 1-2 days. Wait for it.

Not using the APY on idle balances. Any dollars sitting in your Kalshi account earn 3.75-4.05% APY automatically. Users who move money on and off the platform constantly are leaving yield on the table.

Ignoring resolution criteria on sports props. Player prop contracts in particular can have unusual resolution rules around substitutions, injuries, and overtime. Read the criteria before taking large positions.

Trading thin markets without checking depth. Not every market has liquidity. The headline numbers reflect major sports and politics. Niche political contracts or obscure weather markets can have extremely thin order books where your position alone moves the price.

Pros and Cons

Pros

- CFTC regulation and FDIC-insured balances up to $250,000

- Largest prediction market by volume ($12.35B in March 2026)

- Deep sports liquidity across major American leagues

- Fiat onboarding through ACH, wire, and Apple Pay

- 3.75-4.05% APY on idle cash balances

- Integration with Robinhood, Coinbase, and major media outlets

- Institutional-grade infrastructure with sub-10ms VIP execution

- $22 billion valuation signals long-term operational stability

- Clear path for dispute resolution through CFTC

Cons

- Fees higher than Polymarket on most fee-enabled categories

- Sports contracts banned in Massachusetts, legal risk in other states

- Full KYC required for all US users

- Position limits on political contracts ($100K per CFTC rules)

- Debit card deposits carry 2% processing fee

- Less global market coverage than Polymarket International

- Special event maker fees can make longshot strategies uneconomic

- Some resolution criteria feel more legal than intuitive

Is Kalshi Safe?

This comes up constantly and the honest answer is: yes, with the normal caveats that apply to any financial exchange.

Regulatory safety: Kalshi is CFTC-regulated, balances are FDIC-insured to $250,000, and the exchange operates under the same legal framework as CME. If something goes wrong operationally, there is a clear regulatory path. This is the strongest safety profile of any prediction market available to US users.

Operational safety: The company has $22 billion in backing, has survived years of regulatory scrutiny, and has institutional investors who would not tolerate serious operational failures. Not a fly-by-night operation.

Market integrity: Resolution disputes go through CFTC processes rather than decentralised oracle voting. This produces more predictable outcomes than Polymarket’s UMA system, though arguably less creative interpretations on ambiguous markets.

Legal risk: The state-level litigation is the main uncertainty. Sports contracts could be restricted in more states over the coming quarters. Non-sports products appear insulated from this litigation and should remain available everywhere Kalshi is licensed to operate.

For typical retail users, the practical safety profile is comparable to using any major US broker. Your deposits are insured, the exchange has real regulatory oversight, and operational risks are well below those of most offshore competitors.

Final Verdict

Kalshi in April 2026 is a meaningfully different product than it was even 12 months ago. The $22 billion valuation, 1,100% volume growth in 2025, sports expansion, and ongoing state-level litigation have all changed the calculation for users deciding where to trade.

For American retail users, Kalshi is the default answer for prediction markets, and nothing else comes close. The regulatory framework, sports liquidity, fiat infrastructure, and FDIC protection combine to produce a user experience that Polymarket cannot match for US residents. The fee disadvantage is real but usually offset by the idle cash APY and the operational benefits.

For non-US users, Kalshi is usually not the right answer. Polymarket International is cheaper, broader, and does not require KYC. The only users outside the US who should look at Kalshi are those who specifically want American sports markets and find the CFTC framework more comfortable than Polymarket’s offshore structure.

The biggest open question is the state litigation. If Kalshi loses sports contracts in more states, the growth story becomes materially harder. If it wins the preemption argument at the appellate level, the runway is enormous. Both outcomes are genuinely possible, and the stock-level bet on Kalshi is effectively a bet on how the preemption question resolves across the federal court system over the next 18 months.

For now, Kalshi is the strongest prediction market available to US users, and the platform quality reflects the scale of capital and engineering talent behind it. Whether it keeps that position depends on legal outcomes more than product decisions.

Back to full comparison of prediction market platforms

FAQ

Is Kalshi legal in the US?

Yes, Kalshi operates as a CFTC-regulated Designated Contract Market and is legal for US users in almost all states. Sports contracts are currently banned in Massachusetts following a January 2026 preliminary injunction. Other states have ongoing litigation that could result in additional restrictions, but most Kalshi products remain available to most US users as of April 2026.

How much does Kalshi charge in fees?

Kalshi’s taker fee formula is 0.07 × contracts × price × (1 − price). This produces fees that peak at $1.75 per 100 contracts on 50-cent markets and approach zero at the extremes. Maker fees are 0% on standard markets but 0.25% during major events like the Super Bowl and presidential elections. ACH deposits and withdrawals are free; debit card transactions carry a 2% processing fee.

Is Kalshi bigger than Polymarket?

By March 2026 volume, yes. Kalshi processed $12.35 billion compared to Polymarket’s $10.15 billion. However, Polymarket leads in specific categories including politics ($2.97 billion) and crypto ($2.72 billion), while Kalshi dominates sports with 87% of its volume coming from sports contracts.

What is Kalshi’s valuation in 2026?

Kalshi closed a $1 billion Series E in December 2025 at an $11 billion valuation, then raised another $1 billion in March 2026 at a $22 billion valuation. Major investors include Paradigm, Sequoia, Andreessen Horowitz, CapitalG, ARK Invest, and Y Combinator.

Can I use Kalshi in Massachusetts?

You can use Kalshi for politics, economics, weather, and other non-sports markets in Massachusetts. Sports event contracts are currently banned for Massachusetts residents following a January 2026 preliminary injunction that took effect in February 2026. Kalshi is appealing but has not yet restored sports access.

Does Kalshi pay interest on my account balance?

Yes. Kalshi pays 3.75-4.05% APY on idle cash balances in user accounts. This compounds daily and is paid automatically. For users holding larger balances, this substantially offsets trading fees compared to platforms like Polymarket that do not pay interest on idle funds.

How do I deposit money into Kalshi?

Kalshi accepts ACH bank transfers (free, 1-2 business days), wire transfers (free deposit), debit card (2% processing fee), and Apple Pay (free). Users can also deposit cryptocurrency through a ZeroHash partnership, which converts to USD on arrival. The minimum deposit is $1. ACH is the default choice for most users.

Is my money safe on Kalshi?

Kalshi balances are FDIC-insured up to $250,000, and the exchange is CFTC-regulated. This provides stronger protection than any offshore prediction market. Operational risk is comparable to using any US broker, and the company has $22 billion in backing from major institutional investors.

Can you make money on Kalshi?

Yes, but it requires analysis rather than guessing. Profitable Kalshi users typically develop expertise in specific categories like macro economics, sports prop betting, or political forecasting, and they identify mispriced contracts rather than chasing popular narratives. The parabolic fee structure rewards users who trade at the extremes and penalises casual 50-cent coin flips.

Is Kalshi better than DraftKings Predictions?

For serious trading, Kalshi has deeper liquidity, wider market selection, and longer operational history. DraftKings Predictions is available in more states for sports contracts and has better brand recognition among US sports bettors, but the product is newer and less comprehensive. Most active prediction market users who have tried both end up on Kalshi for non-sports contracts and use DraftKings Predictions situationally for sports in states where Kalshi has legal restrictions.

Share

Share

0 views

0 views

Analysis

Analysis  Business

Business  Companies

Companies  Crime

Crime  Finance

Finance  M&A

M&A  Prediction Markets

Prediction Markets  Regulation

Regulation  Reports

Reports  Без рубрики

Без рубрики